Choosing the right life insurance policy is important, and understanding the difference between term and whole life insurance is a valuable part of the decision. At Aflac, we offer a variety of life insurance plans for individuals and families, including term and whole life policies to help meet your specific needs. Read on to learn the differences between term vs. whole life insurance to decide which type of coverage is right for you and your loved ones.

Table of Contents

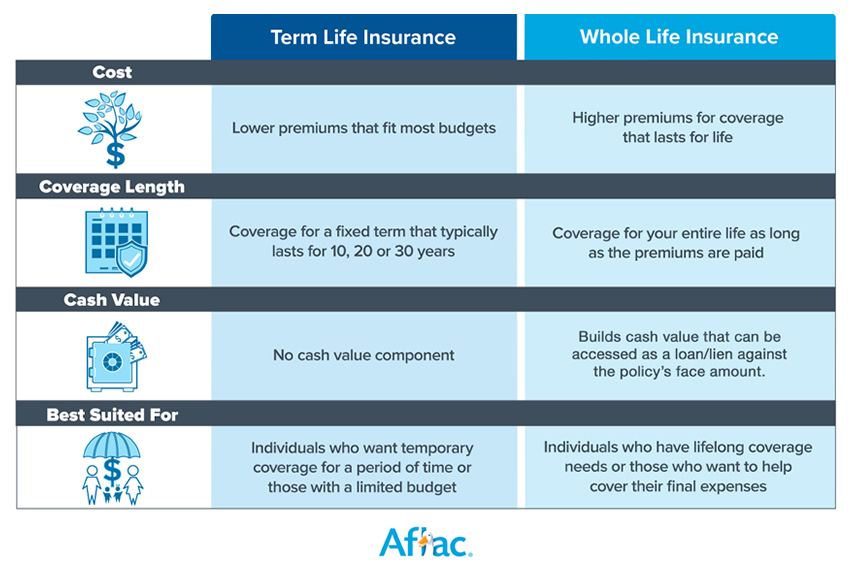

Term life insurance is a temporary policy that provides coverage for a set term or specific amount of time. Here are some key features to keep in mind about this type of policy:

Aflac offers term life insurance for individuals that you can purchase directly. Choose the term length that best works for you based on your unique situation.

Whole life insurance is a permanent policy that provides coverage for your entire life. Here are a few key features of this type of coverage:

Aflac offers whole life insurance for individuals that may give you peace of mind knowing your loved ones can receive financial protection no matter when you pass away. You can purchase a policy directly through Aflac.

There are a few crucial differences in term and whole life insurance. We want to make it easy for you by breaking those differences down into pros and cons.

One of the main differences between whole and term life insurance is the cost. The costs of either plan vary depending on age group, gender, and medical history. Even so, whole life insurance tends to have higher premiums than term life insurance since the payments are put into a cash value account that accumulates over time.

Term life insurance usually has lower premiums. If you choose a 30-year term at a lower rate and your timeline is correct, your family can still receive ample security if you pass away while the policy is active.

Don’t wait until it’s too late. Help cover yourself and your family with coverage from Aflac.

Get StartedWhen deciding whether to get term or whole life insurance, it’s important to consider several factors:

Ultimately, the type of policy you choose should depend on your individual needs and financial circumstances. Consider discussing all your options with a qualified professional who can help you find the right kind of policy for you.

Looking into getting a term life insurance policy? Find out what term life insurance is and its features, rates, and benefits.

Looking into getting a whole life insurance plan? Find out how whole life insurance works and the benefits, costs, pros, and cons.

Looking into getting a term life insurance policy? Find out what term life insurance is and its features, rates, and benefits.

Looking into getting a whole life insurance plan? Find out how whole life insurance works and the benefits, costs, pros, and cons.

1 LIMRA - 2025 Life Insurance Fact Sheet. Published July 26, 2025. https://www.limra.com/siteassets/newsroom/liam/2025/2025_facts_about_life_insurance.pdf. Accessed December 8, 2025.

Content within this article is provided for general informational purposes and is not provided as tax, legal, health, or financial advice for any person or for any specific situation. Employers, employees, and other individuals should contact their own advisers about their situations. For complete details, including availability and costs of Aflac insurance, please contact your local Aflac agent.

Coverage is underwritten by American Family Life Assurance Company of Columbus. In New York, coverage is underwritten by American Family Life Assurance Company of New York.

Aflac life policies - Term & Whole Life (B60000 series): In Arkansas, Oklahoma, Pennsylvania, Texas & Virginia, Policies: ICC18B60C10, ICC18B60100, ICC18B60200, ICC18B60300, & ICC18B60400. Not available in AK, CA, DC, DE, GU, HI, IA, ID, ME, ND, NE, NH, NM, NY, OR, PR, RI, SD, UT, VI or VT. Group Whole Life (Q60000 series): In Arkansas, Delaware & Oregon, Policy Q60100M. In Idaho Policy Q60100MID. In Oklahoma, Policy Q60100MOK. In Pennsylvania, Policy Q60100MPA. In Texas, Policy Q60100MTX. Not available in CA, KS, MA, NY or VA. Group Term Life (Q60000 series): In Arkansas, Idaho, Oklahoma, Oregon & Texas, Policy ICC18Q60200M. In Delaware, Policy Q60200M. Not available in CA, KS, MA, NY or VA.

Aflac Final Expense insurance coverage is underwritten by Tier One Insurance Company, a subsidiary of Aflac Incorporated and is administered by Aetna Life Insurance Company. Tier One Insurance Company is part of the Aflac family of insurers. In California, Tier One Insurance Company does business as Tier One Life Insurance Company (Tier One NAIC 92908). Not available in New York.

Final Expense Life - In Arkansas, Delaware, Idaho, Oklahoma, Oregon, Pennsylvania, Texas, & Virginia, Policies ICC21-AFLLBL21 and ICC21-AFLRPL21; and Riders ICC21-AFLABR22, ICC21-AFLADB22, and ICC21-AFLCDR22. Not available in NY.

Content within this article is provided for general informational purposes and is not provided as tax, legal, health, or financial advice for any person or for any specific situation. Employers, employees, and other individuals should contact their own advisers about their situations. For complete details, including availability and costs of Aflac insurance, please contact your local Aflac agent.

Coverage may not be available in all states. Benefits/premium rates may vary based on state and plan levels. Optional riders may be available at an additional cost. Policies and riders may also contain a waiting period. Refer to the exact policy and rider forms for benefit details, definitions, limitations and exclusions.

Receipt of accelerated death benefits may affect eligibility for public assistance programs. Benefits may also be taxable and are not expected to receive the same favorable tax treatment as other types of accelerated death benefits that may be available.

Aflac | Tier One | WWHQ | 1932 Wynnton Road | Columbus, GA 31999

Aflac New York | 22 Corporate Woods Boulevard, Suite 2 | Albany, NY 12211

Z2200994R3

EXP 1/27